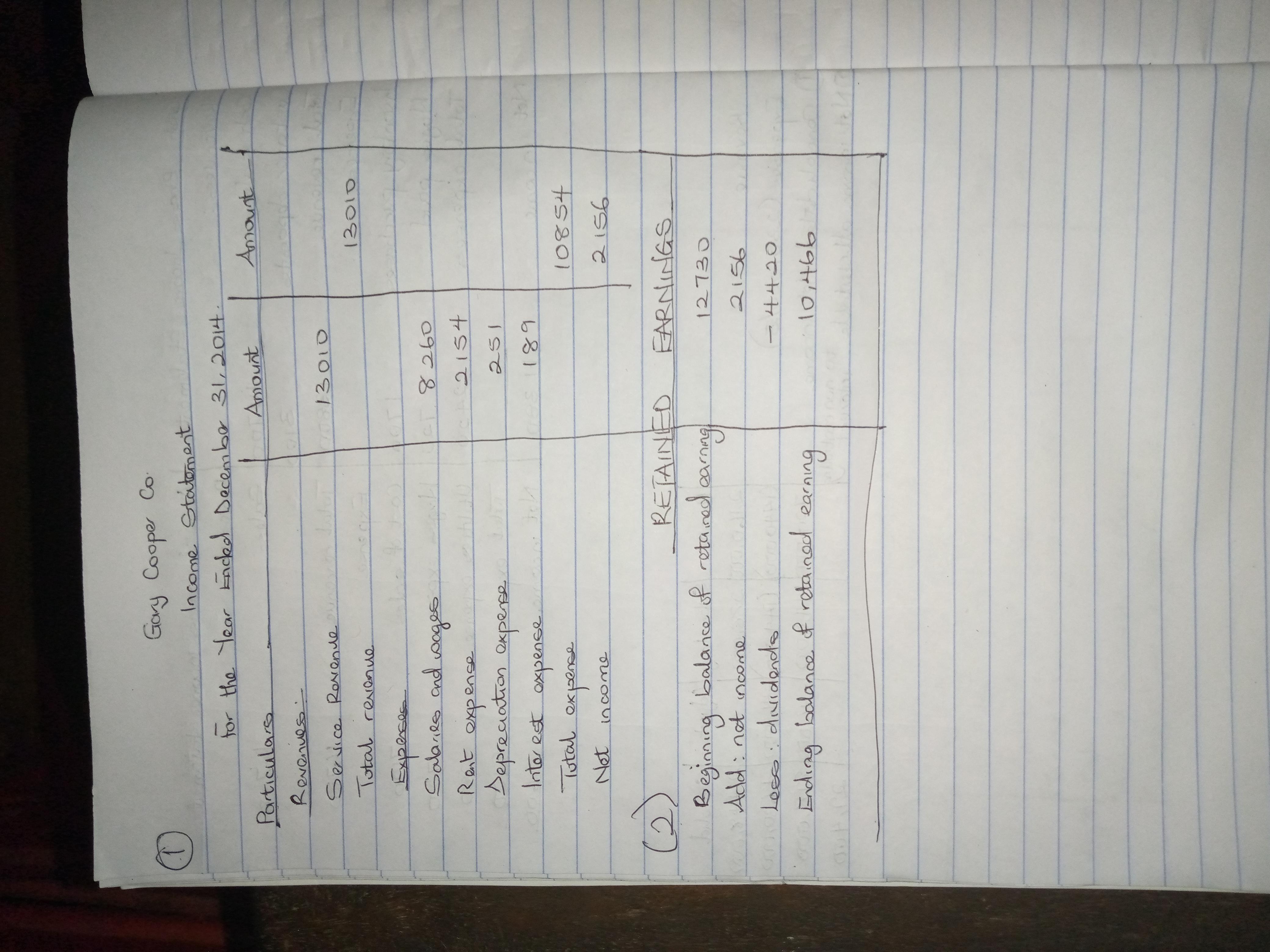

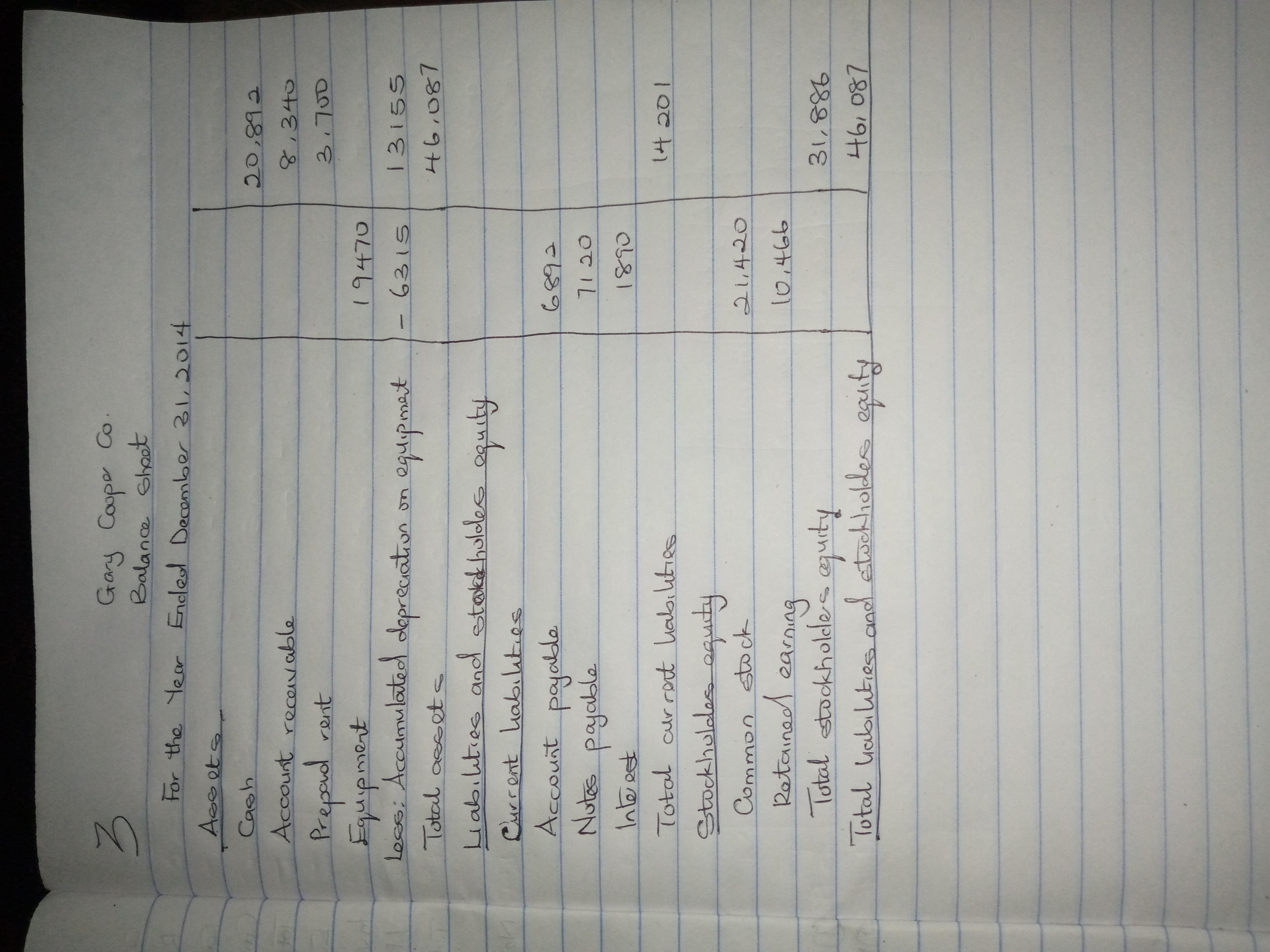

The adjusted trial balance of Gary Cooper Co. as of December 31, 2014, contains the following.

GARY COOPER CO.

ADJUSTED TRIAL BALANCE

DECEMBER 31, 2020

Debit Credit

Cash $20,892

Accounts Receivable 8,340

Prepaid Rent 3,700

Equipment 19,470

Accumulated Depreciation-

Equipment $6,315

Notes Payable 7,120

Accounts Payable 6,892

Common Stock 21,420

Retained Earnings 12,730

Dividends 4,420

Service Revenue 13,010

Salaries and Wages Expense 8,260

Rent Expense 2,154

Depreciation Expense 251

Interest Expense 189

Interest Payable 189

$67,676 $67,676

Instructions:

(a) Prepare an income statement.

(b) Prepare a statement of retained earnings.

(c) Prepare a classified balance sheet.

Answers

Answer: See attachment

Explanation:

An income statement is sometimes referred to as the profit and loss account. It should be noted that it shows the revenue and the expenses that are incurred by a particular company for a certain year.

With regards to the questions above, check the attachments for the solution.

Related Questions

In, & Sons, a small environmental-testing firm, has a small environmental-testing firm, performed 11,400 radon tests for $260 each and 15,000 lead tests for $210 each. Because newer homes are being built with lead-free pipes, lead-testing volume is expected to decrease by 12% next year. However, awareness of radon-related health hazards is expected to result in a 5% increase in radon-test volume each year in the near future. Jim Hart feels that if he lowers his price for lead testing to $200 per test, he will have to face only a 4% decline in lead-test sales in 2018.

Required:

a. Prepare a 2018 sales budget for Hart & Sons assuming that Hart holds prices at 2017 levels.

b. Prepare a 2018 sales budget for Hart & Sons assuming that Hart lowers the price of a lead test to $200.

c. Should Hart lower the price of a lead test in 2018 if the company’s goal is to maximize sales revenue?

Answers

Answer:

A. $5,884,200

B. $5,992,200

C. If the company's aim and objective is for them to maximize their sales revenue then they should go ahead and lower the selling price of lead tests in 2018

Explanation:

a. Preparation of 2018 sales budget for Hart & Sons assuming that Hart holds prices at 2017 levels

Sales budget

For the year ended December 31, 2018

Selling price Units sold Total Revenue

Radon tests

$260 *11,970 =$3,112,200

(11,400 x 1.05 = 11,970)

Lead tests $210*13,200= $2,772,000

(15,000 x 0.88 = 13,200)

(100%-12%=88%)

Total $5,884,200

$3,112,200+$2,772,000

b. Preparation of 2018 sales budget (lower price)

Sales budget

For the year ended December 31, 2018

Selling price Units sold Total Revenue

Radon tests

$260 *11,970 =$3,112,200

(11,400 x 1.05 = 11,970)

Lead tests $200*14,400= $2,880,000

(15,000 x 0.96 = 14,400)

(100%-4%=96%)

Total $5,992,200

$3,112,200+$2,880,000

C. If the company's aim and objective is for them to maximize their sales revenue then they should go ahead and lower the selling price of lead tests in 2018

Your boss would like your help on a marketing research project he is conducting on the relationship between the price of soup and the quantity of soup supplied. He hands you the following document:

Price of Soup Quantity of Soup Supplied

0.50 750

0.75 1,000

1.00 1,500

1.25 2,000

Your task is to take this blank and construct a graphical representation of the data. In doing so, you determine that as the price of soup rises, the quantity of soup supplied increases. This confirms the blank.

For both blanks, the choices are supply curve, quantity of soup supplied, supply schedule, and law of supply. I got law of supply for the first blank, and supply curve for the second blank and I wanted to make sure if I was correct.

Answers

Answer:

Your task is to take this supply schedule and construct a graphical representation of the data. In doing so, you determine that as the price of soup rises, the quantity of soup supplied increases. This confirms the law of supply.

Explanation:

We draw the supply curve being X-axis the quantity and Y-axis the Price.

The date to construct this representation is in the supply schedule.

This confirms the "law of supply" which states that as the price of a good icnrases the willingess to produce more units of that good increases as there is higher revenue.

Sydney Retailing (buyer) and Troy Wholesalers (seller) enter into the following transactions.

May 11 Sydney accepts delivery of $25,000 of merchandise it purchases for resale from Troy: invoice dated. May 11, terms 3/10, n/90, FOB shipping point. The goods cost Troy $16,750. Sydney pays $410 cash to Express Shipping for delivery charges on the merchandise.

12 Sydney returns $1,400 of the $25,000 of goods to Troy, who receives them the same day and restores them to its inventory. The returned goods had cost Troy $938.

20 Sydney pays Troy for the amount owed. Troy receives the cash immediately.

Required:

a. Prepare journal entries that Sydney Retailing (buyer) records for these three transactions.

b. Prepare journal entries that Troy Wholesalers (seller) records for these three transactions.

Answers

Answer:

Buyer

May 11 Dr Merchandise inventory 25,000

Cr Account payable 25,000

Dr Merchandise inventory 410

Cr Cash 410

May 12 Dr Account payable 1400

Cr Merchandise inventory 1400

May 20 Dr Account payable 23,600

Cash 22,892

Dr Merchandise inventory 708

(Seller)

May 11 Dr Account receivable 25,000

Cr Sales revenue 25,000

Dr Cost of goods sold 16,750

Cr Merchandise inventory 16,750

May 12 Dr Sales return and allowance 1400

Cr Account receivable 1400

Dr Merchandise inventory 938

Cr Cost of goods sold 938

May 20 Dr Cash 22,892

Dr Sales discount 708

Cr Account receivable 23,600

Explanation:

Preparation of the Journal entry for Buyer

May 11 Dr Merchandise inventory 25,000

Cr Account payable 25,000

Dr Merchandise inventory 410

Cr Cash 410

May 12 Dr Account payable 1400

Cr Merchandise inventory 1400

May 20 Dr Account payable (25,000-1400) 23,600

Cash (23,600*97%) 22,892

Dr Merchandise inventory 708

(23,600*3%)

Preparation of Journal entry (Seller)

May 11 Dr Account receivable 25,000

Cr Sales revenue 25,000

Dr Cost of goods sold 16,750

Cr Merchandise inventory 16,750

May 12 Dr Sales return and allowance 1400

Cr Account receivable 1400

Dr Merchandise inventory 938

Cr Cost of goods sold 938

May 20 Dr Cash 22,892

[(25,000-14000)*97%]

Dr Sales discount 708

[(25,000-14000)*3%]

Cr Account receivable 23,600

Suppose there is a policy debate over whether the United States should impose trade restrictions on imported ball bearings:________.

Domestic producers of ball bearings send a lobbyist to the U.S. government to request that the government impose trade restrictions on imports of ball bearings. The lobbyist claims that the U.S. ball-bearing industry is new and cannot currently compete with foreign firms. However, if trade restrictions were temporarily imposed on ball bearings, the domestic ball-bearing industry could mature and adjust and would eventually be able to compete in the world market.

Which of the following justifications is the lobbyist using to argue for the trade restriction on ball bearings?

A. Infant-industry argument

B. Saving-domestic-jobs argument

C. Using-protection-as-a-bargaining-chip argument

D. National-security argument

E. Unfair-competition argument

Answers

Answer:

Infant-industry argument

Explanation:

Here is a paraphrased version of the lobbyist's claim and it is from here that we get our answer.

"He claims that this industry in question is new and currently cannot compete with foreign industry".

What this tells us is that this industry in question is an infant industry. An infant industry is a new industry yet to be past it's developmental stage and which cannot be compete yet with other established industries.

Thank you!

If you found my answer useful can I get a brainliest?

Consider a multifactor model with two factors. A well-diversified portfolio (Portfolio P) has a beta of 0.75 on factor 1 and a beta of 1.25 on factor 2. The risk premiums on the factor 1 and factor 2 are 1% and 7%, respectively. The risk-free rate of return is 7%. What is the expected return on portfolio P, according to a two-factor model

Answers

Answer: 16.5%

Explanation:

Expected Return on portfolio P will be calculated as:

= Rf + (Beta1 × F1) + (Beta2 × F2)

where,

Rf = Risk Free rate

F1 = risk premium on Factor1

F2 = risk premium on Factor2

Expected Return will now be:

= 7% + (0.75 × 1%) + (1.25 × 7%)

= 7% + 0.75% + 8.75%

= 16.5%

The expected return on portfolio P, according to a two-factor model will be 16.5%.

Answer:

16.5%

Explanation:

A multi-factor model can be used to explain either an individual security or a portfolio of securities. It does so by comparing two or more factors to analyze relationships between variables and the resulting performance.

DATA

Risk Free rate = Rf = 7%

risk premium on Factor1 = F1 = 1%

Beta (Factor 1) = 1.25

risk premium on Factor2 = F2 = 7%

Beta (Factor 1) = 2

Expected Return = Rf + (Beta1 x F1) + (Beta2 * F2)

Expected Return = 7% + (0.75 x 1%) + (1.25 x 7%)

Expected Return = 0.07 + 0.0075 + 0.0875

Expected Return = 0.165 or 16.5%

In 2009, an 1893 Morgan silver dollar sold for $6,450. Required: What was the rate of return on this investment? (Do not include the percent sign (%). Enter rounded answer as directed, but do not use the rounded numbers in intermediate calculations. Round your answer to 2 decimal places (e.g., 32.16).)

Answers

Answer: 7.86%

Explanation:

Using the Future Value formula;

= Amount * ( 1 + r)^n

The question is looking for the rate so making that the subject would be;

Assuming the car was $1 in 1893,

And n = 2009 - 1893 = 116 years

FV = Amount * ( 1 + r)^n

( 1 + r)^n = FV/ Amount

1 ^n + r^n = FV / Amount

r = n√((FV/ Amount) / 1^n)

r = n√(FV/ Amount)

r = 116√(6,450/ 1)

= 1.07855

Subtract 1 for the percentage;

= 1.07855 - 1

= 7.86%

Sunset Products manufactures skateboards. The following transactions occurred in March. Purchased $24,500 of materials on account. Issued $1,450 of supplies from the materials inventory. Purchased $25,900 of materials on account. Paid for the materials purchased in transaction (1) using cash. Issued $30,900 in direct materials to the production department. Incurred direct labor costs of $29,500, which were credited to Wages Payable. Paid $22,400 cash for utilities, power, equipment maintenance, and other miscellaneous items for the manufacturing shop. Applied overhead on the basis of 120 percent of direct labor costs. Recognized depreciation on manufacturing property, plant, and equipment of $5,900.

The following balances appeared in the accounts of Sunset Products for March:

Beginning Ending

Materials Inventory $ 13,500 ?

Work-in-Process Inventory 24,750 ?

Finished Goods Inventory 97,500 $ 54,750

Cost of Goods Sold 120,000

Required:

a. Prepare journal entries to record the transactions. (If o entry is required for a transaction/event, select "No journal entry required" in the first account field.)

Transactions General Journal Debit Credit

1.

2.

3.

4.

5.

6.

7.

8.

9.

b. Prepare T-accounts to show the flow of costs during the period from Materials Inventory through Cost of Goods Sold.

Materials Inventory

Beg. bal. ___________ ____________

______ ___________ ____________ ______

______ ___________ ____________ ______

______ ___________ ____________ ______

End. bal. ___________ ____________ ______

Work in Progress Inventory

Beg. bal. ___________ ____________

______ ___________ ____________ ______

______ ___________ ____________ ______

______ ___________ ____________ ______

______ ___________ ____________ ______

End. bal. ___________ ____________ ______

Manufacturing Overhead Control

Beg. bal. ___________ ____________

______ ___________ ____________ ______

______ ___________ ____________ ______

______ ___________ ____________ ______

______ ___________ ____________ ______

End. bal. ___________ ____________ ______

Applied Manufacturing Overhead

Beg. bal. ___________ ____________

______ ___________ ____________ ______

______ ___________ ____________ ______

End. bal. ___________ ____________ ______

Accounts Payable

Beg. bal. ___________ ____________

______ ___________ ____________ ______

______ ___________ ____________ ______

______ ___________ ____________ ______

End. bal. ___________ ____________ ______

Cash

Beg. bal. ___________ ____________

______ ___________ ____________ ______

______ ___________ ____________ ______

______ ___________ ____________ ______

End. bal. ___________ ____________ ______

Wages Payable

Beg. bal. ___________ ____________

______ ___________ ____________ ______

______ ___________ ____________ ______

End. bal. ___________ ____________ ______

Accumulated Depreciation-Property, Plant, and Equipment

Beg. bal. ___________ ____________

______ ___________ ____________ ______

______ ___________ ____________ ______

End. bal. ___________ ____________ ______

Finished Goods Inventory

Beg. bal. ___________ ____________

Goods Completed ___________ ____________ Transfer to Cost of Goods Sold

End. bal. ___________ ____________

Cost of Goods Sold

Beg. bal. ___________ ____________

Finished Goods Inventory ___________ ____________

End. bal. ___________ ____________

Answers

Answer:

Sunset Products

a) Journal Entries:

Transactions General Journal Debit Credit

Materials Inventory $24,500

Accounts Payable $24,500

To record the purchase of materials on account.

Manufacturing Overhead $1,450

Materials Inventory $1,450

To record the issue of supplies.

Materials Inventory $25,900

Accounts Payable $25,900

To record the purchase of materials on account.

Accounts Payable $24,500

Cash Account $24,500

To record the payment on account.

Work-in-Process Inventory $30,900

Materials Inventory $30,900

To record the issue of direct materials to the production department.

Work-in-Process Inventory $29,500

Factory Wages $29,500

To record direct labor costs to work in process.

Manufacturing Overhead $22,400

Cash Account $22,400

To record the payment for utilities and other expenses.

Work-in-Process Inventory $35,400

Manufacturing Overhead $35,400

To apply overhead to work in process.

Manufacturing Overhead $5,900

Depreciation Expense $5,900

To recognize depreciation on property, plant, and equipment.

Manufacturing overhead applied $29,750

Manufacturing overhead $29,750

To transfer manufacturing overhead to the overhead applied account.

b) T-accounts:

Materials Inventory

Transaction Details Debit Credit

Beginning balance $ 13,500

Accounts Payable 24,500

Manufacturing overhead $1,450

Accounts Payable 25,900

Work-in-Process Inventory 30,900

Ending balance $31,550

Work-in-Process Inventory

Transaction Details Debit Credit

Beginning balance $24,750

Materials Inventory 30,900

Factory Wages 29,500

Manufacturing Overhead 35,400

Finished Goods Inventory $71,600

Ending balance 54,200

Finished Goods Inventory

Transaction Details Debit Credit

Beginning balance $97,500

Work-in-Process 71,600

Cost of goods sold $114,350

Ending balance 54,750

Cost of Goods Sold

Transaction Details Debit Credit

Beginning balance $120,000

Overapplied overhead $5,650

Ending balance 114,350

Manufacturing Overhead Control Account

Transaction Details Debit Credit

Materials Inventory $1,450

Cash Account 22,400

Depreciation expense 5,900

Manufacturing overhead applied $29,750

Manufacturing Overhead Applied

Transaction Details Debit Credit

Work in Process $35,400

Manufacturing overhead $29,750

Overapplied overhead 5,650

Accounts Payable

Transaction Details Debit Credit Materials Inventory $24,500

Materials Inventory 25,900

Cash Account $24,500

Ending Balance 25,900

Cash Account

Transaction Details Debit Credit

Accounts Payable $24,500

Manufacturing Overhead 22,400

Explanation:

a) Data and Calculations:

Accounts balances of Sunset Products for March:

Beginning Ending

Materials Inventory $ 13,500 ?

Work-in-Process Inventory 24,750 ?

Finished Goods Inventory 97,500 $ 54,750

Cost of Goods Sold 120,000

The following events took place for Rushmore Biking Inc. during February, the first month of operations as a producer of road bikes:

Purchased $400,000 of materials.

Used $362,100 of direct materials in production.

Incurred $104,200 of direct labor wages.

Applied factory overhead at a rate of 42% of direct labor cost.

Transferred $483,700 of work in process to finished goods.

Sold goods with a cost of $460,300.

Revenues earned by selling bikes, $761,600.

Incurred $154,800 of selling expenses.

Incurred $75,300 of administrative expenses.

Required:

Prepare the income statement for Rushmore Biking for the month ending February 28

Answers

Answer: See attachment

Explanation:

Note that in the attachment,

Gross profit was the difference between the revenue and the cost of goods sold. This is:

= 761600 - 460300

= 301300

The selling and administrative expenses was the addition of the selling expense and the administrative expenses.

Check the attachment for further details.

Which section of a CAR Residential Purchase Agreement is a provision divided into three sections: mediation, arbitration of disputes, and additional terms?

Answers

Answer: Appraisal contingency and Removal.

Explanation:

The appraisal contingency, is a kind of CAR residential purchase agreement, which allows a buyer to back out of the deal if the house appraises for less than the already agreed-upon value. and the loan contingency, this term lets the buyer back out if he/she can't get their loan approved for the said purposes.

The section of a car residential purchase agreement that separates it into three sections would be:

Section 9C

The section titled 9C functions to separate the property purchase provisions into three varied divisions. These divisions include mediation followed by arbitration of disputes, and the external terms that fulfill the remaining ones.The other options are present in order to fulfill if either of them fails to resolve the dispute.Thus, "section 9C" is the correct answer.

Learn more about "Residential Agreement" here:

brainly.com/question/10539028

You are CEO of Rivet Networks, maker of ultra-high performance network cards for gaming computers, and you are considering whether to launch a new product. The product, the Killer X3000, will cost $900,000 to develop up front (year 0), and you expect revenues the first year of $800,000, growing to $1.5 million the second year, and then declining by 40% per year for the next 3 years before the product is fully obsolete. In years 1 through 5, you will have fixed costs associated with the product of $100,000 per year, and variable costs equal to 50% of revenues.

A. What are the cash flows for the project in years 0 through 51

B. Plot the NPV profile for this nvestment using discount rates from 0% to 50% in 5% increments.

C. What is the project's NPV if the project's cost of capital is 10%?

D. Use the NPV profile to estimate the cost of capital at which the project would become unprofitable; that is, estimate the project's IRR or calculate it using the data.

Initial investment $900,000

Revenues vear 1 $800,000

Revenues vear 2 $1,500,000

Revenues decline years 4000

Fixed costs vears 1-5 $100,000

Variable costs 50%

Answers

Answer:

F= (900,000)

F1= 300,000

F2 = 650,000

F3 = 350,000

F4 = 170,000

F5 = 62,000

NPV at 10% $327487

IRR 20.587%

Explanation:

F0 -900,000

revenues variable cost fixed cost net flow

F1 800,000 -400000 -100,000 = 300,000

F2 1,500,000 -750000 -100,000 = 650,000

F3 900000 -450000 -100,000 = 350,000

F4 540000 -270000 -100,000 = 170,000

F5 324000 -162000 -100,000 = 62,000

NPV at 10%:

For each cashflow, we apply the discount of a lump sum formula

[tex]\frac{Maturity}{(1 + rate)^{time} } = PV[/tex]

And add them together for the net present value

[tex]\left[\begin{array}{ccc}Year&$cashflow&PV\\0&-900,000&-900,000\\1&300,000&272,727\\2&650,000&537,190\\3&350,000&262,960\\4&170,000&116,112\\5&62,000&38,497\\Total&&327487\\\end{array}\right][/tex]

We solve for the IRR using the excel IRR formula

we list the cashflow and use IRR to select them.

Read the overview below and complete the activities that follow. In addition to trade accounts payable, many companies have other types of current liabilities. These include amounts withheld from employees' pay, sales and other taxes payable, deposits, and other accrued liabilities.

CONCEPT REVIEW:

Companies have many different types of current liabilities. These can include various taxes payable (income tax, sales tax, payroll tax), accrued amounts for salary, vacation or other benefits, and estimates such as accrued utilities and warranty. To adhere to the concept of the matching principle, companies must estimate the amount of their other liabilities.

1. Federal anid state governments do not specily the exact______to be maint, but do specify the amounts to be withheld.

2. Income taxes withheld from employees but not yet submitted to the govenment are considered to be a(n)______.

3. When testing customer deposits, auditors typically review a(n)______of the individual deposits.

4. When testing other accrued liabilities. auditors may independently calculate the amount and______ it to management's estimate.

5. Property tax payments are typically______in number.

Answers

Answer:

1. Federal and state governments do not specify the exact__number of accounts____to be maintained, but do specify the amounts to be withheld.

2. Income taxes withheld from employees but not yet submitted to the government are considered to be a(n)_liability_____.

3. When testing customer deposits, auditors typically review a(n)_sample_____of the individual deposits.

4. When testing other accrued liabilities. auditors may independently calculate the amount and__compare____ it to management's estimate.

5. Property tax payments are typically_numerous_____in number.

Explanation:

Even Federal and State governments and business organizations apply the matching principle of the generally accepted accounting principles. The principle requires that revenues are matched to the expenses that are incurred in generating them and vice versa. The purpose is to present a balance view of financial performance and position of the reporting entity. For this reason, who expenses may not be actually paid for and they are recognized while some that have been paid for are not. The same rule applies to the revenue side.

Environmental recovery company RexChem Part- ners plans to finance a site reclamation project that will require a 4-year cleanup period. The company plans to borrow $1.8 million now. How much will the company reveice in annual paymebts

Answers

Complete question Text:

Environmental recovery company RexChem Partners plans to finance a site reclamation project that will require a 4-year cleanup period. The company will borrow $1.8 million now to finance the project. How much will the company have to receive in annual payments for 4 years, provided it will also receive a final lump sum payment after 4 years in the amount of $800,000? The MARR is 10% per year on its investment

Answer:

We are going to receive annual payment of $395,471

Explanation:

We solve for the present value of the lump-sum today:

PRESENT VALUE OF LUMP SUM

[tex]\frac{Maturity}{(1 + rate)^{time} } = PV[/tex]

Maturity 800,000.00

time 4.00

rate 0.1

[tex]\frac{800000}{(1 + 0.1)^{4} } = PV[/tex]

PV 546,410.76

Now, we deduct this fromthe 1,800,000 loan:

1,800,000 - 546,410.76 = 1,253,589.24

this value will be the amount the yearly installment will ghave to pay.

Installment of a present annuity

[tex]PV \div \frac{1-(1+r)^{-time} }{rate} = C\\[/tex]

PV 1,253,589.24 €

time 4

rate 0.1

[tex]1253589.24 \div \frac{1-(1+0.1)^{-4} }{0.1} = C\\[/tex]

C $ 395,470.805

Exercise 2-8 Preparing T-accounts (ledger) and a trial balance LO P2 Following are the transactions of a new company called Pose-for-Pics Aug. 1 Madison Harris, the owner, invested $6,see cash and $33,509 of photog company paid $2,100 cash for an insurance policy covering the next 24 month:s s The company purchased office supplies for $888 cash. 20 The company received $3,331 cash in photography fees earned. 31 The company paid $675 cash for August utilities.

Required:

1. Post the transactions to the T-accounts.

2. Use the amounts from the T-accounts in Requirement (1) to prepare an August 31 trial balance for Pose-for-Pics. Complete this question by entering your answers in the tabs below.

Required 1 Required 2

Post the transactions to the T-accounts Cash ies Balance

Answers

Answer:

Pose-for-Pics

1. T-accounts:

Cash Account

Date Accounts Titles Debit Credit

Aug. 1 Common Stock $6,500

Aug. 1 Prepaid Insurance $2,100

Aug. 1 Supplies 888

Aug. 20 Service Revenue 3,331

Aug. 31 Utilities Expense 675

Aug. 30 Ending balance $6,168

Common Stock

Date Accounts Titles Debit Credit

Aug. 1 Cash $6,500

Aug. 1 Equipment 33,509

Aug. 30 Ending Balance $40,009

Photography Equipment

Date Accounts Titles Debit Credit

Aug. 1 Common Stock $33,509

Prepaid Insurance

Date Accounts Titles Debit Credit

Aug. 1 Cash $2,100

Supplies

Date Accounts Titles Debit Credit

Aug. 1 Cash $888

Service Revenue

Date Accounts Titles Debit Credit

Aug. 20 Cash $3,331

Utilities Expense

Date Accounts Titles Debit Credit

Aug. 31 Cash $675

2. Pose-for-Pics

TRIAL BALANCE

As of August 31

Accounts Titles Debit Credit

Cash $6,168

Common Stock $40,009

Photography Equipment 33,509

Prepaid Insurance 2,100

Supplies 888

Service Revenue 3,331

Utilities Expense 675

Totals $43,340 $43,340

Explanation:

Correctly posting the transactions of Pose-for-Pics to the general ledger ensures that the two sides of the Trial Balance are equal as of August 31. The balanced Trial Balance assures the arithmetical accuracy of the entries and postings in the general ledger. This trial balance will then form the basis for preparing the financial statements after effecting the necessary adjusting entries.

Which best describes the difference in the duties of restaurant employees who work inside and outside a kitchen?

O Kitchen workers clear tables and wash dishes, while the other restaurant employees take orders and prepare and

cook the food.

O Kitchen workers answer phones and handle advertising, while the other restaurant employees prepare drinks and

set tables.

O Kitchen workers greet guests and take orders, while the other restaurant employees prepare and cook food and

clean dishes.

o Kitchen workers prepare and cook food and clean dishes, while the other restaurant employees greet guests and

take orders

Answers

Answer:

Kitchen workers prepare and cook food and clean dishes, while the other restaurant employees greet guests and take orders.

Explanation:

Kitchen workers prepare and cook food and clean dishes, while the other restaurant employees greet guests and take orders is the best describes the difference in the duties of restaurant employees who work inside and outside a kitchen. Hence, option D is correct.

What are duties and responsibilities of restaurant staff?The tasks and obligations of a waiter or waitress include greeting and seating customers, collecting their orders, properly relaying them to the kitchen, and memorizing the menu in order to suggest additional appetizers, desserts, or drinks.

The duties of an assistant manager in a restaurant range from scheduling shifts to taking care of the needs of the personnel. They must also guarantee that the establishment complies with all relevant rules and encourages a pleasant dining experience with top-notch customer service.

promptly, expertly, and amiably handled customers' orders for food and beverages. Good menu knowledge was used to help clients and, when possible, upsell menu items. Ensured that everything was kept orderly and clean at all times, including the placement of all tables and silverware.

Thus, option D is correct.

For more information about duties and responsibilities of restaurant staff, click here:

https://brainly.com/question/28644430

#SPJ5

One-year Treasury securities yield 4.85%. The market anticipates that 1 year from now, 1-year Treasury securities will yield 5.2%. If the pure expectations theory is correct, what is the yield today for 2-year Treasury securities

Answers

Answer:

5.025%

Explanation:

When we assume that the pure expectations theory is correct, then we are assuming that there is no risk premium involved. The formula to determine the yield for the 2 year treasury security:

(1 + i)² = (1 + 4.85%) x (1 + 5.2%)

(1 + i)² = 1.0485 x 1.052

(1 + i)² = 1.103022

√(1 + i)² = √1.103022

1 + i = 1.050248542

i = 0.050248542 = 5.025%

Assume you make monthly deposits of $200 starting one month from now into an account that pays 6% per year, compounded semiannually. If you want to know how much you will have after four years, the value of i you should use in the F/A factor, assuming no interperiod interest, is

Answers

Answer:

3%

Explanation:

the account pays a 6% annual rate, but since it is compounded semiannually, you must divide it by 2 = 6% / 2 = 3%

since no interperiod interest is paid, the semiannual payment = $200 x 6 = $1,200

the future value = $1,200 x 8.8923 (FV annuity factor, 3%, 8 periods) = $10,670.76

Firms often seek to borrow money to expand their capital stock, and the price they pay for the money is the interest rate. What happens to quantity of money demanded if the interest rate increases

Answers

Answer:

When interest rate rises, the quantity of money demanded reduces

Explanation:

As interest rate increases firms seeking to borrow money for capital stock expansion are likely not going to go ahead with it. The reason is simply because, interest rate and money demanded have an inverse relationship. As interest rate rises money demanded falls because it means that for any amount of money borrowed the interest rate attached to it is higher making the cost of borrowing heavier on the borrower.

Leonard, a company that manufactures explosionproof motors, is considering two alternatives for expanding its international export capacity. Option 1 requires equipment purchases of $900,000 now and $560,000 two years from now, with annual M&O costs of $79,000 in years 1 through 10. Option 2 involves subcontracting some of the production at costs of $280,000 per year beginning now through the end of year 10. Neither option will have a significant salvage value.

Required:

Use a present worth analysis to determine which option is more attractive at the company’s MARR of 20% per year. (Note: Check out the spreadsheet exercises for new options that Leonard has been offered recently.)

Answers

Answer:

Since the total present value of Option 2 of – $1,453,892 is lower than the total present value of Option 1 of – $1,620,094, it implies that Option 2 costs less and more attractive at the company’s MARR of 20% per year than Option 1. Therefore, Option 2 should be selected.

Explanation:

Note: See the attached excel file for the calculation of the total present values (in bold red color) of the two alternatives for expanding international export capacity.

Present worth can be described as an equivalence method of analysis in which the cash flows of an investment or a project are discounted to a single present value.

From the attached excel file, we have:

Total present value of Option 1 = – $1,620,094

Total present value of Option 2 = – $1,453,892

Since the total present value of Option 2 of – $1,453,892 is lower than the total present value of Option 1 of – $1,620,094, it implies that Option 2 costs less and more attractive at the company’s MARR of 20% per year than Option 1. Therefore, Option 2 should be selected.

Sunset Products manufactures skateboards. The following transactions occurred in March. Purchased $24,500 of materials on account. Issued $1,450 of supplies from the materials inventory. Purchased $25,900 of materials on account. Paid for the materials purchased in transaction (1) using cash. Issued $30,900 in direct materials to the production department. Incurred direct labor costs of $29,500, which were credited to Wages Payable. Paid $22,400 cash for utilities, power, equipment maintenance, and other miscellaneous items for the manufacturing shop. Applied overhead on the basis of 120 percent of direct labor costs. Recognized depreciation on manufacturing property, plant, and equipment of $5,900.

The following balances appeared in the accounts of Sunset Products for March:

Beginning Ending

Materials Inventory $ 13,500 ?

Work-in-Process Inventory 24,750 ?

Finished Goods Inventory 97,500 $ 54,750

Cost of Goods Sold 120,000

Required:

a. Prepare journal entries to record the transactions. (If o entry is required for a transaction/event, select "No journal entry required" in the first account field.)

Transactions General Journal Debit Credit

1.

2.

3.

4.

5.

6.

7.

8.

9.

b. Prepare T-accounts to show the flow of costs during the period from Materials Inventory through Cost of Goods Sold.

Materials Inventory

Beg. bal. ___________ ____________

______ ___________ ____________ ______

______ ___________ ____________ ______

______ ___________ ____________ ______

End. bal. ___________ ____________ ______

Work in Progress Inventory

Beg. bal. ___________ ____________

______ ___________ ____________ ______

______ ___________ ____________ ______

______ ___________ ____________ ______

______ ___________ ____________ ______

End. bal. ___________ ____________ ______

Manufacturing Overhead Control

Beg. bal. ___________ ____________

______ ___________ ____________ ______

______ ___________ ____________ ______

______ ___________ ____________ ______

______ ___________ ____________ ______

End. bal. ___________ ____________ ______

Applied Manufacturing Overhead

Beg. bal. ___________ ____________

______ ___________ ____________ ______

______ ___________ ____________ ______

End. bal. ___________ ____________ ______

Accounts Payable

Beg. bal. ___________ ____________

______ ___________ ____________ ______

______ ___________ ____________ ______

______ ___________ ____________ ______

End. bal. ___________ ____________ ______

Cash

Beg. bal. ___________ ____________

______ ___________ ____________ ______

______ ___________ ____________ ______

______ ___________ ____________ ______

End. bal. ___________ ____________ ______

Wages Payable

Beg. bal. ___________ ____________

______ ___________ ____________ ______

______ ___________ ____________ ______

End. bal. ___________ ____________ ______

Accumulated Depreciation-Property, Plant, and Equipment

Beg. bal. ___________ ____________

______ ___________ ____________ ______

______ ___________ ____________ ______

End. bal. ___________ ____________ ______

Finished Goods Inventory

Beg. bal. ___________ ____________

Goods Completed ___________ ____________ Transfer to Cost of Goods Sold

End. bal. ___________ ____________

Cost of Goods Sold

Beg. bal. ___________ ____________

Finished Goods Inventory ___________ ____________

End. bal. ___________ ____________

Answers

Answer:

Sunset Products

a) Journal Entries:

Transactions General Journal Debit Credit

Materials Inventory $24,500

Accounts Payable $24,500

To record the purchase of materials on account.

Manufacturing Overhead $1,450

Materials Inventory $1,450

To record the issue of supplies.

Materials Inventory $25,900

Accounts Payable $25,900

To record the purchase of materials on account.

Accounts Payable $24,500

Cash Account $24,500

To record the payment on account.

Work-in-Process Inventory $30,900

Materials Inventory $30,900

To record the issue of direct materials to the production department.

Work-in-Process Inventory $29,500

Factory Wages $29,500

To record direct labor costs to work in process.

Manufacturing Overhead $22,400

Cash Account $22,400

To record the payment for utilities and other expenses.

Work-in-Process Inventory $35,400

Manufacturing Overhead $35,400

To apply overhead to work in process.

Manufacturing Overhead $5,900

Depreciation Expense $5,900

To recognize depreciation on property, plant, and equipment.

Manufacturing overhead applied $29,750

Manufacturing overhead $29,750

To transfer manufacturing overhead to the overhead applied account.

b) T-accounts:

Materials Inventory

Transaction Details Debit Credit

Beginning balance $ 13,500

Accounts Payable 24,500

Manufacturing overhead $1,450

Accounts Payable 25,900

Work-in-Process Inventory 30,900

Ending balance $31,550

Work-in-Process Inventory

Transaction Details Debit Credit

Beginning balance $24,750

Materials Inventory 30,900

Factory Wages 29,500

Manufacturing Overhead 35,400

Finished Goods Inventory $71,600

Ending balance 54,200

Finished Goods Inventory

Transaction Details Debit Credit

Beginning balance $97,500

Work-in-Process 71,600

Cost of goods sold $114,350

Ending balance 54,750

Cost of Goods Sold

Transaction Details Debit Credit

Beginning balance $120,000

Overapplied overhead $5,650

Ending balance 114,350

Manufacturing Overhead Control Account

Transaction Details Debit Credit

Materials Inventory $1,450

Cash Account 22,400

Depreciation expense 5,900

Manufacturing overhead applied $29,750

Manufacturing Overhead Applied

Transaction Details Debit Credit

Work in Process $35,400

Manufacturing overhead $29,750

Overapplied overhead 5,650

Accounts Payable

Transaction Details Debit Credit Materials Inventory $24,500

Materials Inventory 25,900

Cash Account $24,500

Cash Account

Transaction Details Debit Credit

Accounts Payable $24,500

Manufacturing Overhead 22,400

Explanation:

a) Data and Calculations:

Accounts balances of Sunset Products for March:

Beginning Ending

Materials Inventory $ 13,500 ?

Work-in-Process Inventory 24,750 ?

Finished Goods Inventory 97,500 $ 54,750

Cost of Goods Sold 120,000

A competitive firm maximizes profit by choosing a level of output where the world price is equal to the firm's

Answers

Answer: c. Marginal Cost

Explanation:

A Competitive firm operates in a market where they are price takers. This means that the price they charge is equal to both their average revenue and their Marginal Revenue.

P = MR = AR

Companies maximise profit at a point where Marginal Revenue equals Marginal Cost because at this point, resources are being fully utilized.

If the Competitive firm's Price is the same as its Marginal Revenue this means that to maximise profits, the firm should choose an output level where the price is equal to the marginal cost.

Following are account balances (in millions of dollars) from a recent FedEx annual report, followed by several typical transactions. Assume that the following are account balances on May 31, 2014:

Property and equipment (net) $15,543

Retained earnings 12,716

Accounts payable 1702

Prepaid expenses 329

Accrued expenses payable 1894

Long-term notes payable 1667

Other noncurrent assets 3557

Common stock ($0. 10 par value) 32

Receivables $4,581

Other current assets 610

Cash 2328

Spare parts, supplies, and fuel 437

Other noncurrent liabilities 5616

Other current liabilities 1286

Additional paid-in capital 2472

These accounts are not necessarily in good order and have normal debit or credit balances. Assume the following transactions (in millions) occurred the next year ending May 31, 2015:

a. Provided delivery service to customers, receiving $21,704 in accounts receivable and $17,600 in cash.

b. Purchased new equipment costing $3,434; signed a long-term note.

c. Paid $13,864 cash to rent equipment and aircraft, with $10,136 for rental this year and the rest for rental next year.

d. Spent $3,864 cash to maintain and repair facilities and equipment during the year.

e. Collected $24,285 from customers on account.

f. Repaid $350 on a long-term note (ignore interest).

g. Issued 20 shares of additional stock for $16.

h. Paid employees $15,276 during the year.

i. Purchased for cash and used $8,564 in fuel for the aircraft and equipment during the year.

j. Paid $784 on accounts payable. Ordered $88 in spare parts and supplies.

Answers

Question Completion:

Prepare the necessary journal entries without the narration.

Answer:

FedEx

a. Debit Cash $17,600

Debit Accounts Receivable $21,704

Credit Service Revenue $39,304

b. Debit Equipment $3,434

Credit Note Payable (long-term) $3,434

c. Debit Rent Expense $10,136

Debit Prepaid Rent $3,728

Credit Cash Account $13,864

d. Debit Maintenance Expense $3,864

Credit Cash Account $3,864

e. Debit Cash Account $24,285

Credit Accounts Receivable $24,285

f. Debit Long-term Notes Payable $350

Credit Cash Account $350

g. Debit Cash Account $320

Credit Common Stock $2

Credit Additional paid-in capital $318

h. Debit Salaries and Wages Expense $15,276

Credit Cash Account $15,276

i. Debit Spare parts, supplies, and fuel Expense $8,564

Credit Cash Account $8,564

j. Debit Accounts Payable $784

Credit Cash Account $784

k. No journal is required.

Explanation:

With the above journal entries, the accountants at FedEx have recorded the listed business transactions for the first time in the accounts of FedEx. From the entries, these transactions will then be posted to the general ledger where accounts, transactions, and business events are summarized.

Following are several figures reported for Allister and Barone as of December 31, 2015:

Allister Barone

Inventory $50,000 $300,000

Sales 1,000,000 8,00,000

Investment income Not given

Cost of goods sold 500,000 400,000

Operating expenses 230,000 300,000

Allister acquired 90 percent of Barone in January 2020. In allocating the newly acquired subsidiary's fair value at the acquisition date, Allister noted that Barone had developed a customer list worth $66,000 that was unrecorded on its accounting records and had a six-year remaining life. Any remaining excess fair value over Barone's book value was attributed to goodwill. During 2021, Barone sells inventory costing $135,000 to Allister for $190,000. Of this amount, 20 percent remains unsold in Allister's warehouse at year-end.

Determine balances for the following items that would appear on Allister's consolidated financial statements for 2015:

a. Inventory

b. Sales

c. Cost of Goods Sold

d. Operating Expenses

e. Net Income Attributable to Non-controlling Interest

Answers

Answer:

a. $344,500

b. $1,610,000

c. $405,500

d. $530,000

e. $9,550 loss

Explanation:

First, Eliminate the Intragroup transactions as follows :

Elimination Journal for the Intragroup Sale :

Sales (Barone) $190,000 (debit)

Cost of Sales (Allister) $190,000 (credit)

Elimination of unrealized profit in closing inventory :

Cost of Sales (Barone) $5,500 (debit)

Inventory (Allister) $5,500 (credit)

Unrealized Profit in Inventory ($190,000 - $135,000) × 10% = $5,500

Then, Consolidate the Financial Statements taking into account the elimination journals

Note : Consolidation is 100% of Parent + 100% of Subsidiary.

Note : A firm that is exercising control (> 50% Voting Rights) is required to prepare Consolidated Financial Statements - IFRS 3.

Consolidated Income Statement

Sales (1,000,000 + 8,00,000 - $190,000) $1,610,000

Cost of Sales ( $500,000 + 400,000 - $190,000 + $5,500) ($715,500)

Gross Profit $894,500

Less Operating Expenses ($230,000 + $300,000) ($530,000)

Net Income $364,500

Consolidated Financial Statement (Extract)

Inventory ($50,000 + $300,000 - $5,500) $344,500

Subsidiary Profit

Net Income Attributable to Non-controlling Interest

Net Income Attributable to Non-controlling Interest = Net Subsidiary Income × % Non Controlling Interest

Net Subsidiary Income - Barone

Sales (800,000 - 190,000) $610,000

Less Cost of Sales ( 400,000 + 5,500) ($405,500)

Gross Profit $204,500

Less Operating Expenses ($300,000)

Net Income/ (loss) ($95,500)

Therefore,

Net Income Attributable to Non-controlling Interest = ($95,500) × 10%

= $9,550 loss

Assume that the following events occurred at a division of Generic Electric for March of the current year:

1. Purchased $100 million in direct materials.

2. Incurred direct labor costs of $46 million.

3. Determined that manufacturing overhead was $76 million.

4. Transferred 90 percent of the materials purchased to work-in-process.

5. Completed work on 75 percent of the work-in-process. Costs are assigned equally across all work-in-process.

6. The inventory accounts have no beginning balances. All costs incurred were debited to the appropriate account and credited to Accounts Payable.

Required:

Give the amounts for the following items in the Work-in-process account: (Do not round your intermediate calculations. Enter your final answers in millions rounded to 2 decimal places.)

Transfers-In ____ Million

Transfers-Out ______ Million

Ending Balance _____ Million

Answers

Answer:

A. Transfer -In= $212,000,000

B. Transfer-Out = $159,000,000

C. Ending balance= $53,000,000

Explanation:

a) Calculation for Transfers-In

Transfer -In=$46,000,000 + $76,000,000 + (.90× $100,000,000)

Transfer -In=$46,000,000 + $76,000,000 + $90,000,000

Transfer -In= $212,000,000

b) Calculation for Transfer-Out

Transfer-Out=.75 × $212,000,000

Transfer-Out = $159,000,000

c) Calculation for the ending balance

Using this formula

Ending balance=Transfer -In-Transfer-Out

Let plug in the formula

Ending balance= $212,000,000 - $159,000,000 Ending balance= $53,000,000

Wainwright Corporation owns and operates a wholesale warehouse.

The following transactions occurred during March 2016:

1. Issued 30,000 shares of capital stock in exchange for $300,000 in cash.

2. Purchased equipment at a cost of $40,000. $10,000 cash was paid and a note payable was signed for the balance owed.

3. Purchased inventory on account at a cost of $90,000. The company uses the perpetual inventory system.

4. Credit sales for the month totaled $120,000. The cost of the goods sold was $70,000.

5. Paid $5,000 in rent on the warehouse building for the month of March.

6. Paid $6,000 to an insurance company for fire and liability insurance for a one-year period beginning April 1, 2016.

7. Paid $70,000 on account for the merchandise purchased in 3.

8. Collected $55,000 from customers on account.

9. Recorded depreciation expense of $1,000 for the month on the equipment.

Required:

1.Analyze each transaction and classify each as a financing, investing and/or operating activity.

A transaction can represent more than one type of activity.

Also indicate the cash effect of each, if any.

Activities:

Transaction Financing Investing Operating

1

2

3

4

5

6

7

8

9

Answers

Answer:

Wainwright Corporation

Activities:

Transaction Financing Investing Operating Cash Effect

1. Common Stock Issue $300,000 $300,000

Transaction Financing Investing Operating Cash Effect

2. Equipment purchase $40,000 -$10,000

Transaction Financing Investing Operating Cash Effect

3. Inventory purchase $90,000

Transaction Financing Investing Operating Cash Effect

4. Credit Sales $120,000

Transaction Financing Investing Operating Cash Effect

5. Rent Expense $5,000 -$5,000

Transaction Financing Investing Operating Cash Effect

6. Prepaid Insurance $6,000 -$6,000

Transaction Financing Investing Operating Cash Effect

7. Accounts Payable payment $70,000 -$70,000

Transaction Financing Investing Operating Cash Effect

8. Cash Receipt from customers $55,000 $55,000

Transaction Financing Investing Operating Cash Effect

9. Depreciation Expense $1,000 None

Explanation:

These transactions of Wainwright Corporation in March 2016 are classified as financing, investing, or operating activities. Some have cash effect, while others did not have any effect on the cash asset of the company. Some cash effects are negative, representing outflows while others are positive, representing inflows. The outflows are marked with the minus sign while the inflows are not marked. This analysis shows that every transaction can be classified into financing, investing, or operating activities according to the presentation of the statement of cash flows but not all have cash effects.

Assume that on January 1, 2012, a parent company acquired a 70% interest in a subsidiary's voting common stock. On the date of acquisition, the fair value of the subsidiary's net assets equaled their reported book values except for machinery and equipment, which had a fair value of $480,000 and a reported book value of $250,000. The machinery and equipment had a 5 year remaining useful life and no salvage value. The following are the highly summarized pre-consolidation income statements of the parent and subsidiary for the year ended December 31 , 2013:

Income Statement Parent Subsidiary

Revenues $2,160,000 $288,000

Equity income 60,200

Expenses 1440000 144,000

Net income $780,200 144,000

For the year ended December 31, 2013, what amounts will be reported for (1) consolidated net income and (2) net income attributable to the non-controlling interest, respectively, in the parent's consolidated financial statements?

Answers

Answer: 1. $818,000

2. Check attachment

Explanation:

1. The amounts that will be reported for consolidated net income will be $818,000.

(2) Note that for the net income attributable to the non-controlling interest, respectively, in the parent's consolidated financial statements was calculated as:

= ($144,000 - $46,000) × 30%

= $98,000 × 0.3

= $29400

Kindly check the attachment for more analysis.

Angela is selling her car through a newspaper advertisement. When she finds a buyer, she wants a form of payment which is guaranteed to be good. Which form of payment should she AVOID? *

Personal check

Certified check

Cashier's check

Cash

Answers

Formation of Corporation with Transfer of Property from Several Shareholders at Different Times (LO. 1, 7)Jane, Jon, and Clyde incorporate their respective businesses and form Starling Corporation. On March 1 of the current year, Jane exchanges her property (basis of $50,000 and fair market value of $150,000) for 150 shares in Starling Corporation. On April 15, Jon exchanges his property (basis of $70,000 and fair market value of $500,000) for 500 shares in Starling. On May 10, Clyde transfers his property (basis of $90,000 and fair market value of $350,000) for 350 shares in Starling.a. If the three exchanges are part of a pre-arranged plan, who will recognize a gain on the exchanges?SelectOnly ClydeOnly JaneAll of the partiesNone of the partiesCorrect 1 of Item 1.b. Now assume that Jane and Jon exchanged their property for stock four years ago, while Clyde transfers his property for 350 shares in the current year. Clyde's transfer is not part of a pre-arranged plan with Jane and Jon to incorporate their businesses.Clyde will recognize a gain of $ on the transfer.c. Returning to the original facts, assume the property that Clyde contributes has a basis of $490,000 (instead of $90,000). Why would it be better from a tax perspective for Clyde to wait to transfer his property rather than be a part of Jane's and Jon's transfers?

Answers

Answer: See explanation

Explanation:

a. If the three exchanges are part of a pre-arranged plan, it should be noted that none of them will recognize a gain on the exchanges. Here, my the non-recognition provision applies.

b. Based on the scenario in the question, Clyde will recognize a gain of the amount of the difference between the market value and the basis. This will be:

= $350,000 – $90,000

= $260,000

c. This is because Clyde's loss will be recognized. The loss here will be: = $350,000 - $490,000 = -$140,000.

provide an example of two companies that have built an effective co-operation.briefly explain the relationship of it g

Answers

Answer:

An example of two companies that have built an effective co-operation is discussed below in details.

Explanation:

Louis Vuitton & BMW

Co-operation Operations: The Art of Travel

Designer Louis Vuitton and Carmaker BMW may not be the usual simple pairings. But if you believe about it, they have some significant things in general. If you concentrate on Louis Vuitton's trademark baggage lines, they're both in the industry of journey. They both value leisure. And finally, they're both well-known, fabulous brands that are recognized for high-quality craftsmanship.

Shannon’s Brewery is a newly opened micro-brewery of craft beers located about a mile from Samantha Springs in Keller, Texas. According to Shannon Carter, (owner, founder, and brew master) Samantha Springs "is an exceptional water source." "It’s surrounded by a very unique rock formation that has very, very hard compressed rocks that have been hollowed out with this very fine sand. The water travels for miles, and the end product is this filtered water that is just phenomenal." Shannon Carter crafts what the brew master calls "wholesome beers" made with the highest quality, non-GMO grains and malts available and brewed using techniques garnered from his Irish heritage. Shannon’s mission statement closely reflects this philosophy. According to Shannon Carter:

Our award-winning beer is brewed with the best stuff on earth: pure spring water, whole grain, whole flower hops and a whole lotta love! For us, "brewed with the best stuff on earth," is much more than a saying. it’s a guiding principle. Paramount to this commitment is our multi-step fire-brewed process.

Required:

What makes Shannon’s beer great?

Answers

Answer:

Marketing Mix

Explanation:

What makes Shannon's beer great is basically her Marketing Mix. This combination of aspects is what ultimately makes Shannon's beer unique and attracts a large number of customers which makes it very profitable. This includes a combination of a unique beer recipe with high-quality ingredients, a top-notch mission statement, dedicated marketing that focuses on the organic and wholesome features of the product, and lastly a dedicated customer base that loves all of these features and purchases the product. This marketing mix sets Shannon's Beer apart from the competition and makes it great.

After visiting several automobile dealerships, Richard selects the used car he wants. He likes its $10,000 price, but financing through the dealer is no bargain. He has $2,000 cash for a down payment, so he needs an $8,000 loan. In shopping at several banks for an installment loan, he learns that interest on most automobile loans is quoted at add-on rates. That is, during the life of the loan, interest is paid on the full amount borrowed even though a portion of the principal has been paid back. Richard borrows $8,000 for a period of four years at an add-on interest rate of 11 percent. What is the total interest on Richard’s loan? What is the total cost of the car? What is the monthly payment? What is the annual percentage rate (APR)?

Answers

Answer:

A. $3,520

B. $13,520

C. $240 monthly

D. 21.55%

Explanation:

A. Calculation for the total interest

Using this formula

Interest = (Principal) (Rate) (Time)

Let plug in the formula

Interest = (8000)(.11)(4)

Interest = $3,520

B. Calculation for the total cost of the car

Using this formula

Total Cost = Down Payment + Principal amount Borrowed + Interest amount

Let plug in the formula

Total Cost = $2,000 + $8,000 + $3,520

Total Cost = $13,520

C. Calculation for the monthly payment

Using this formula

Monthly Payment = (Principal amount Borrowed + Total interest amount ) / Total number of payments

Monthly Payment = ($8,000 + $3,520) / 48

Monthly Payment=$11,520/48

Monthly Payment=$240 monthly

Note 4-year * 12 months will give us 48months

D. Calculation for the annual percentage rate (APR) using this formula

APR= (2 × n × I) / [P × (N + 1)]

Let plug in the formula

APR = (2 × 12 × $3,520) / [$8,000 × (48+1)]

APR =$84,480/$8,000×49

APR=$84,480/$392,000

APR=0.2155×100

APR= 21.55%